Salary or dividends? The 2026/27 director's dilemma — and a free calculator

If you run your own limited company, one question comes back every year: how should you actually pay yourself? Salary, dividends, or some blend of the two — and how much of the profit should you take at all?

The honest answer is “it depends” — on your other income, whether you can claim the Employment Allowance, how many associated companies you have, whether you want to top up a pension, and what you’re trying to optimise for. So we built a calculator that works it out for you, for the 2026/27 tax year. You can try it here:

This article explains what’s changed this year, the thinking the tool encodes, and a couple of non-obvious results it tends to surface.

What changed for 2026/27

Two things make this year worth a fresh look:

- Dividend tax went up. Following the Autumn Budget 2025, the ordinary and upper dividend rates each rose by 2 percentage points from 6 April 2026. For 2026/27 dividends are taxed at 10.75% (basic band), 35.75% (higher) and 39.35% (additional), after a £500 tax-free dividend allowance. That narrows the long-standing gap between salary and dividends and makes the “take everything as dividends” reflex less automatic.

- Thresholds are still frozen. The Personal Allowance (£12,570), the basic-rate limit and the employer NI secondary threshold remain frozen to April 2031. More of your income drifts into higher rates each year by stealth, so deliberate planning matters more, not less.

The classic answer — and why £12,570

For most owner-managed companies the efficient structure is still a modest salary plus dividends:

- A salary up to the £12,570 Personal Allowance is free of income tax, and because it also matches the NI primary threshold it carries no employee National Insurance either.

- Salary is deductible against corporation tax, so every pound reduces the company’s CT bill.

- If your company can claim the Employment Allowance (more on that below), the employer NI on that salary is wiped out too.

So £12,570 is the textbook sweet spot: tax-free to you, deductible for the company, and it secures a qualifying year towards your State Pension. Profits beyond that are then taken as dividends, up to wherever your plan calls for stopping.

Where it gets complicated

The £12,570-plus-dividends rule of thumb is a good start, but several real-world factors move the answer:

- Employment Allowance (£10,500). A sole director who is the only employee paid over the £5,000 secondary threshold cannot claim it. Add a second director or employee paid above that threshold and the company can — which changes the salary maths materially.

- Corporation tax marginal relief. Profits between £50,000 and £250,000 are effectively taxed at a 26.5% marginal rate (19% below, 25% above). Those limits are divided by the number of associated companies, so a group of companies can push you into the marginal band at much lower profit.

- Other income. Rental income, a pension, or a second salary all use up your bands first, so dividends stack on top at higher rates — and the optimal split shifts accordingly.

- A qualifying NI year. If the pure optimum would put your salary below the £6,708 Lower Earnings Limit, you can lose a year towards your State Pension. The tool can floor your salary at the LEL to protect it — at no NI cost.

- Pensions. An employer pension contribution is corporation-tax deductible and NI-free, often the cheapest way to extract value if you don’t need the cash now.

- You don’t have to take it all. Sometimes the right move is to retain profit in the company (taxed only at the CT rate) rather than pay 35.75% dividend tax to get it out today.

The calculator weighs all of these together, and lets you optimise for one of three goals: the most tax-efficient plan (stay within the basic-rate band), a specific target take-home, or extract everything this year.

The husband-and-wife angle

A favourite for owner-managed companies run by couples: with two directors, you get two Personal Allowances, two basic-rate bands and two dividend allowances — and, because two directors are paid above the secondary threshold, the £10,500 Employment Allowance becomes available.

There’s a subtler result the tool will prove for you. When the company sits in the corporation-tax marginal band, a salary sheltered by the Employment Allowance can actually beat dividends — right up to the point where the £10,500 allowance is used up (around £40,000 of salary each). Outside the marginal band, or where higher salaries would tip a director over £100,000 and start tapering their Personal Allowance, it pays to stay low. The calculator searches for that crossover rather than guessing, and splits the dividends between the two of you for the lowest combined tax.

A worked example

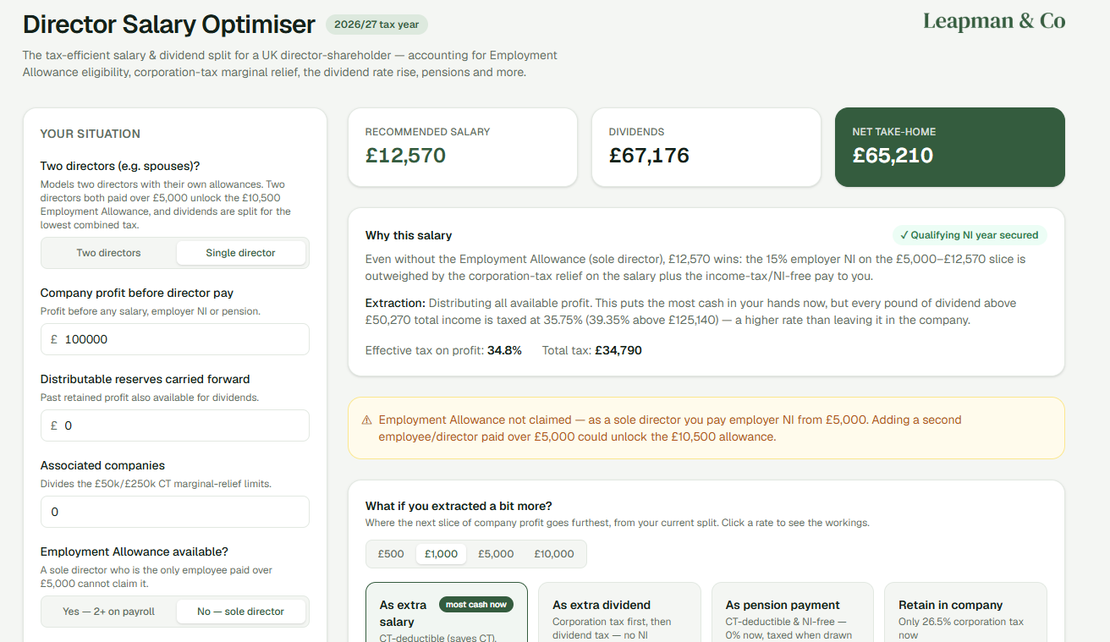

Take a single director with £100,000 of company profit and the Employment Allowance available. The efficient plan is a £12,570 salary, with dividends taken up to the basic-rate ceiling and the surplus retained or pensioned. If instead you distribute everything this year, the calculator shows a net take-home of roughly £65,700 — and, crucially, the exact tax cost of that last slice of dividends, so you can see whether it’s worth taking or better left in the company.

That “what does the next £1,000 actually cost me?” view is the part most rules of thumb miss.

Try it

The calculator is free, runs entirely in your browser, and is built specifically for 2026/27 rates and thresholds:

It’s a planning aid, not a substitute for advice. Everyone’s circumstances differ — particularly around associated companies, pension allowance tapers and the timing of distributions — so do confirm the plan with us before you act. If you’d like us to run your specific numbers and build the full extraction strategy around them, get in touch.

This article is for general information and does not constitute tax advice. Figures reflect published 2026/27 rates for England, Wales and Northern Ireland; Scottish income-tax bands differ.